:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/OIRCZYY4X5F3XKXSEPA4VVCPJA.jpg)

Before last week's price crash really got underway, there was a brief crash in the price of ether on Tuesday, Feb. 22. The TradeBlock ETX, a spot reference rate for ETH, fell 15%, from about $1,765 to $1,534 in just over half an hour, before recovering almost as quickly. It was notable because it broke one of the most liquid markets in crypto.

The Feb. 22 ETH sell-off came with larger than usual volume on all four of the exchanges that are components of the ETX. One of these exchanges, Kraken, experienced a "flash crash," a rapid and anomalous drop in price. Flash crashes aren't entirely uncommon in crypto – Binance experienced one on Friday when it was hit with a sudden influx of orders for Polkadot trading contracts – but Kraken's was extremely notable since it saw ETH-U.S. dollar trades as low as $700, less than half the lowest price printed on any other ETX component exchange.

An analysis of the Kraken ETH flash crash is inconclusive as to whether it was caused by a technical glitch. However, TradeBlock data shows that trading activity on Kraken wasn't much different from what two comparable ETX component exchanges saw in the lead-up to the crash, which happened at 9:18 a.m. ET (2:18 p.m. UTC). [TradeBlock is a subsidiary of CoinDesk.] The analysis shines a light on the fragmented nature of crypto market structure, where market disruptions affect even the most liquid assets, even under normal market dynamics. CoinDesk reached out to Kraken for comment, but did not receive any statement in time for publication.

What happened, tick-by-tick

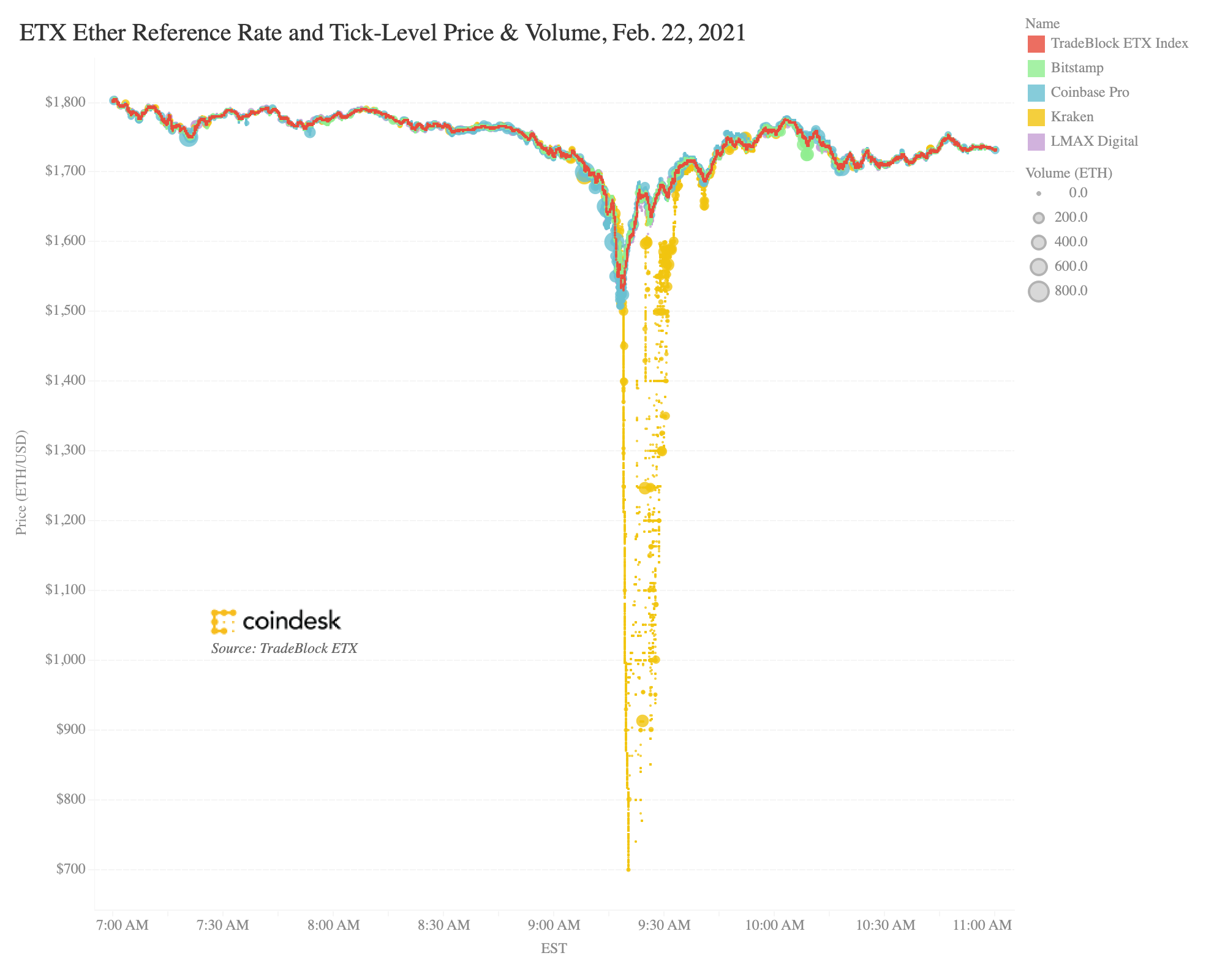

The Kraken ETH flash crash: tick-level price and volume

The chart above tracks the ETX ether price, alongside trades printed on each of the four exchanges that make up the ETX. Right up to about 9:18 a.m. ET, all four exchanges and the ETX reference rate are moving in sync, in what looks like a fairly normal ether price dip. The increasing size of the bubbles represents larger and larger trades as traders react to the price action, one way or another. At 9:18 a.m., the Kraken market, represented in yellow, suddenly crashes severely. Its trades drop out of the ETX calculation as it continues for the next 15 minutes or so to print trades way out of line with the rest of the market.

These four exchanges represent the most liquid ETH-USD markets that are accessible to U.S. investors. Kraken's CEO has said the Kraken ETH flash crash was not the result of a technical glitch. As the following three charts will show, however, two comparable ETX component exchanges handled comparable increases in volume just fine, including the usually lower-volume ETH-USD market on Bitstamp. The ETX incorporates only executed trades, not orders.

Kraken volumes were high, not highest

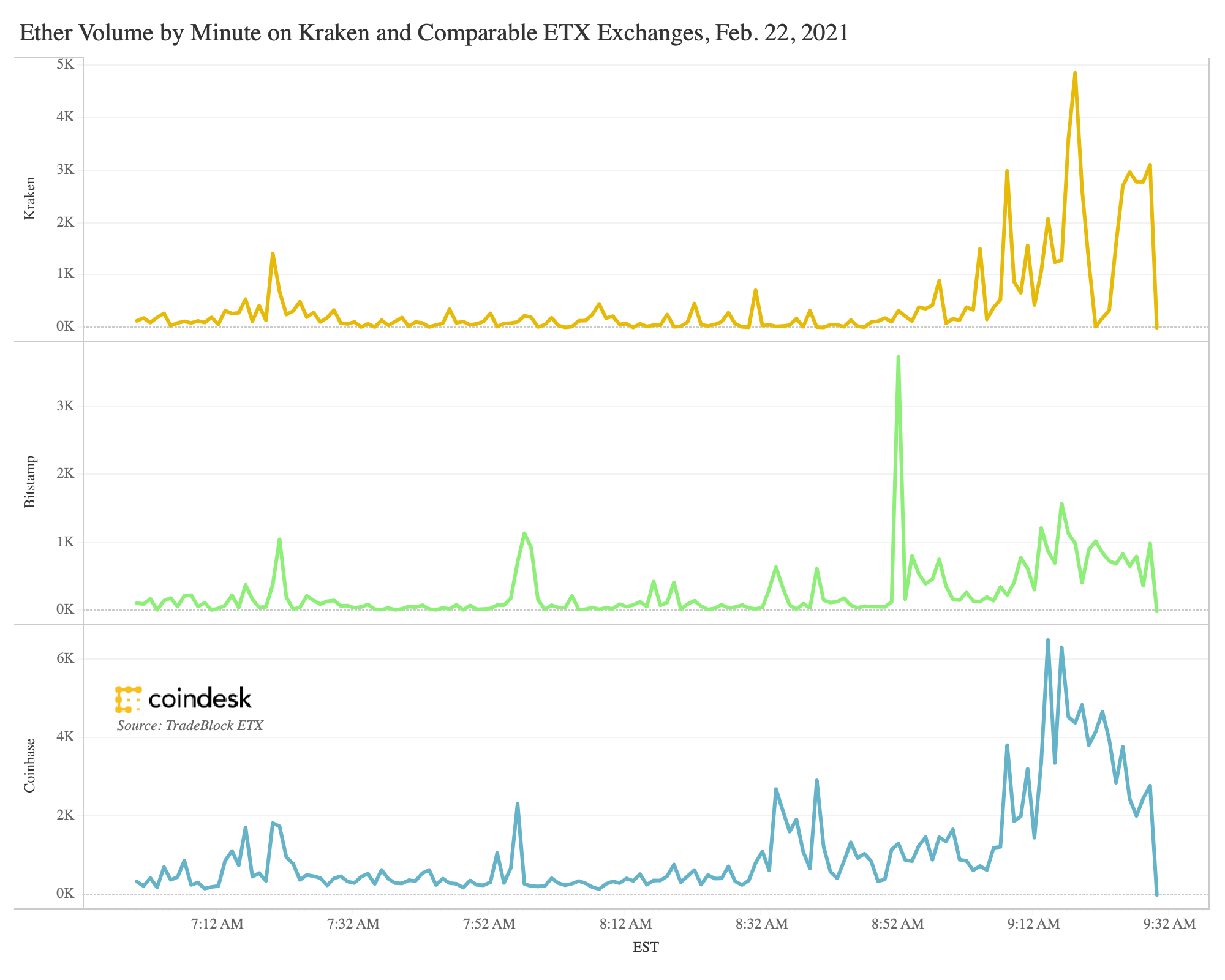

Ether volume by minute on Kraken and comparable ETX component exchanges during the Kraken ETH flash crash.

The yellow, green and blue lines in the chart above show minute-by-minute volume on Bitstamp, Coinbase and Kraken. LMAX, the fourth ETX component exchange, is excluded because it represents exclusively institutional volume. The others are a mix of institutional and retail activity.

The surge in volume on Kraken that preceded its ETH flash crash was not the largest of the three exchanges, nor was it a greater outlier compared with normal ETH-USD activity on the exchange.

Kraken printed the largest trade

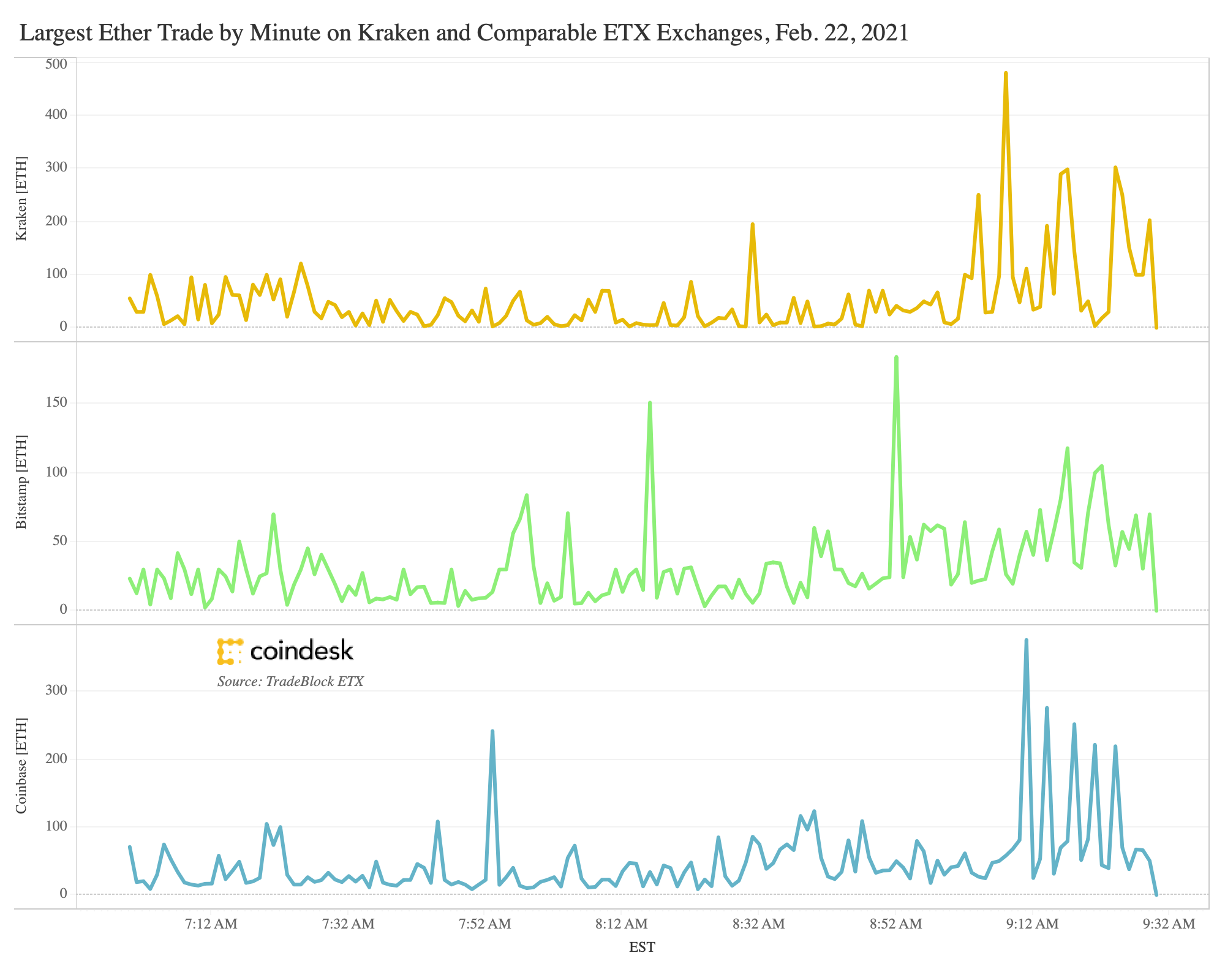

Volume of the largest ETH-USD trades by minute on Kraken and comparable ETX component exchanges during the Kraken ETH flash crash.

Kraken did, however, see the largest single ETH-USD transaction of the three, represented by a spike in the yellow line that's well above other large trades that morning. It was a 481.4 ETH trade executed at 9:08 a.m. ET, just as the ETX reference rate had slid to a hair above $1,700, and about 10 minutes before Kraken prices dove so far below the average. That could have been the culprit that dried up the order book, but it's not such an outlier that it looks conclusive. Coinbase's largest trade, seen on the blue line at 9:11 a.m. ET, was 376.7 ETH. Bitstamp's was 184.1 ETH, at 8:52 a.m. ET.

A surge in large trades

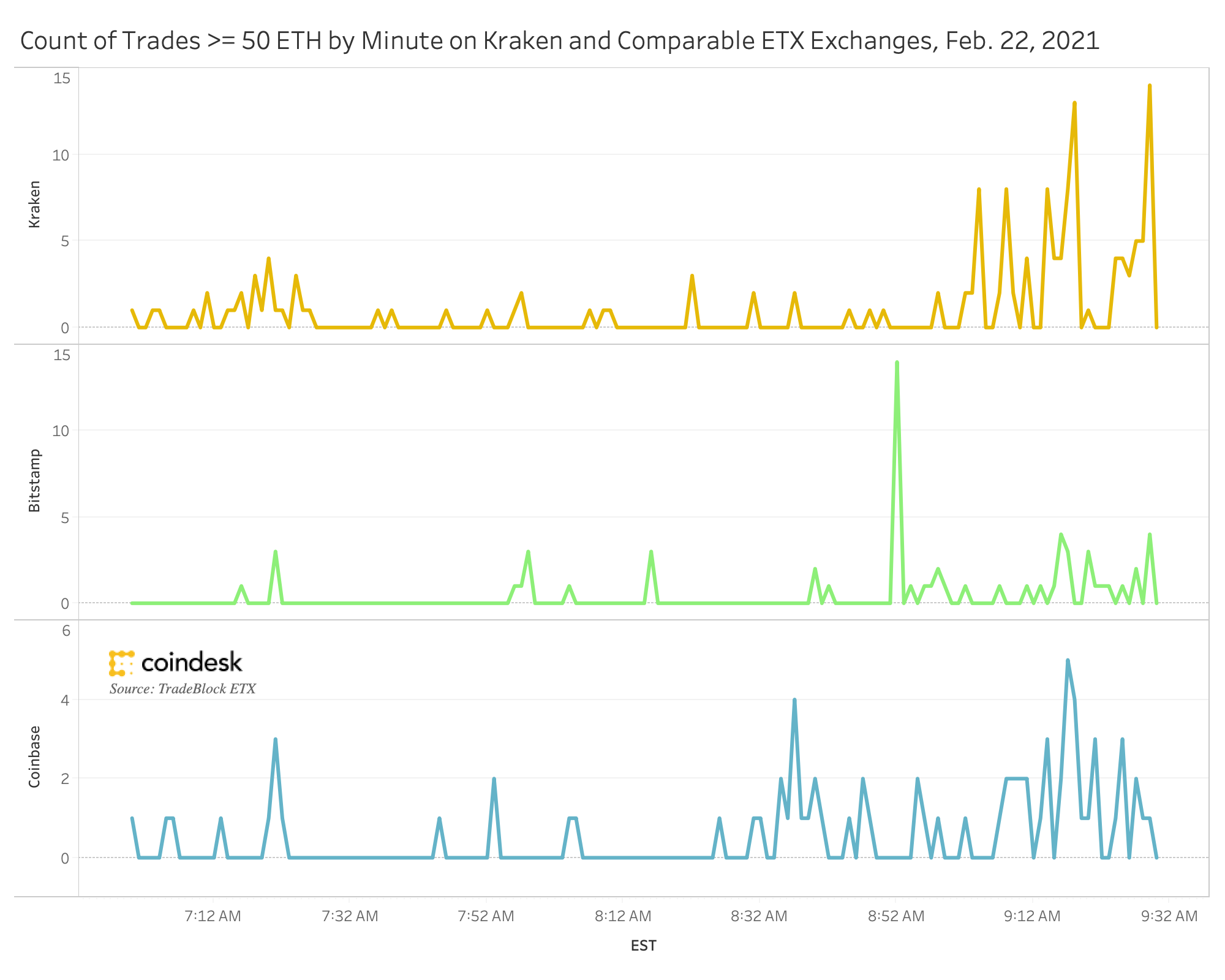

Count of trades >= 50 ETH by minute on Kraken and comparable ETX component exchanges during the Kraken ETH flash crash.

Were there other large trades? Yes. At 9:18 a.m. ET, as the Kraken ETH flash crash began, Kraken handled 13 trades in volume of 50 ETH or greater. That's significantly more large ETH trades than any other market at that time. However, it wasn't the highest count of large ETH trades on the morning of Feb. 22. At 8:52 a.m. ET, Bitstamp printed 14 transactions of 50 ETH or more. By 9:29 a.m. ET, Kraken would match that number, presumably as arbitrage traders took advantage of the still-wide spread between prices printed on Kraken and the rest of the market, as represented by the ETX.

As noted above, the ETX counts only executed trades. This is to prevent manipulation of the reference rate through order-book activities like "spoofing," a kind of manipulative activity in which traders place disingenuous orders, to simulate demand. If it's order-book analysis you're looking for, Kaiko has a good breakdown of the Kraken ETH flash crash, along those lines.

Kaiko didn't find any conclusive evidence as to what caused the crash, either. Whether it was a technical glitch or a sudden run on the order book probably doesn’t matter. With price discovery taking place on multiple venues, technology risk is multiplied and liquidity is divided. Until capital is able to flow more freely into these fragmented markets, investors should expect more flash-crash events.

DISCLOSURE

Please note that our privacy policy, terms of use, cookies, and do not sell my personal information has been updated.

The leader in news and information on cryptocurrency, digital assets and the future of money, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups. As part of their compensation, certain CoinDesk employees, including editorial employees, may receive exposure to DCG equity in the form of stock appreciation rights, which vest over a multi-year period. CoinDesk journalists are not allowed to purchase stock outright in DCG.

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/PFEHNV7HU5CCPFROJKQIPWNYJU.jpg)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/YLVK7NL7PJAVRJVREC7DTR6XME.jpg)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/EXPOIBREMFHSHA7CVOGJ5TDWUY.jpg)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/PJTR3KRDWJCRVE3QREM6KUOK7A.png)