:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/HI2P6X4YYFEAXFXOLBS2WZTCQY.jpg)

Nikhilesh De is CoinDesk's managing editor for global policy and regulation. He owns marginal amounts of bitcoin and ether.

Stablecoins seem to be the vector by which the U.S. will implement regulations on cryptocurrencies directly. A hearing in the House of Representatives will bring this potentially one step closer to reality.

You’re reading State of Crypto, a CoinDesk newsletter looking at the intersection of cryptocurrency and government. Click here to sign up for future editions.

Talking stablecoins

The narrative

The House Financial Services Committee, after holding a substantive discussion on crypto regulation broadly in December, is turning its attention to stablecoins specifically. The committee will discuss last year’s President’s Working Group report on stablecoins with one of the report’s authors, homing in on the recommendations and how they might be implemented.

Why it matters

Today’s hearing might bring us another step closer to legislation on digital assets. And as has been hinted more and more over the past year, this legislation might focus on stablecoins.

Breaking it down

The House Financial Services Committee will host a hearing on stablecoins at 10:00 a.m. Eastern time today, focusing on a report by the President’s Working Group for Financial Markets that recommends lawmakers pass a law to treat stablecoin issuers as regulated bank-like institutions.

As of press time, the sole witness will be Nellie Liang, under secretary for domestic finance at the Treasury Department, who worked on the report.

Liang told CoinDesk in November the current regulatory framework in place does not address the potential risks posed by stablecoins, hence the report’s recommendation that Congress pass a law specifically addressing stablecoin regulation.

She reiterated her views in prepared testimony published Monday night, outlining the risks and recommendations identified in the report.

The report, published Nov. 1, 2021, recommended Congress require that stablecoins and payment stablecoin arrangements be under the jurisdiction of a federal prudential framework, such as by treating stablecoin issuers like insured depository institutions.

It also recommended that unregulated entities be barred from issuing stablecoins

“We focused on prudential risks,” Liang said last year. “We mean the risk that investors could run on a stablecoin, if they were to lose confidence in the reserve assets that are backing the stablecoin … there could be risks to the payment system because of disruption in stablecoins in how they're stored or transferred.”

Indeed, a hearing memo published Thursday night references last year’s iron titanium token run. This past June, investors sold the TITAN token en masse after concerns that it had no real liquidity. The TITAN token was part of the collateral for the IRON stablecoin. The run on TITAN led to IRON losing its peg to the U.S. dollar, falling below 70 cents within hours.

IRON did not regain its peg until September, according to CoinMarketCap.

Possible legislation

One member of the committee, Rep. Josh Gottheimer (D-N.J.), has begun circulating a draft discussion bill that would enact some of the recommendations from the report ahead of Tuesday’s hearing, according to Politico.

“The committee's going to be active this year on this,” he told the news outlet. “I'm hearing there's a lot of interest."

According to the draft bill, any nonbank stablecoin issuers would have to ensure their circulating stablecoins are fully backed by reserves, and some issuers may be required to maintain more than 100% of their supply in reserves if the Treasury secretary orders it.

These reserves can only be held in U.S. dollars or securities issued by the federal government, unless the secretary allows for another reserve asset.

Moreover, these assets would have to be kept in insured accounts at a depository institution.

In suggesting these requirements, the draft bill would appear to go beyond the report’s recommendations. While the report does recommend that any legislation create a framework for federal oversight of stablecoin issuers, limited issuance and “maintenance of reserve assets,” and ensure that any framework include provisions to oversee stablecoin transactions and end users as well as issuers, the report did not mention a specific reserve requirement.

The report did specify that a federal supervisor be appointed.

Spokespeople for Gottheimer did not return requests for comment.

Ron Hammond, the director of government relations at the Blockchain Association, an industry lobbying group, tweeted that Gottheimer is not alone in how he sees the report's recommendations.

However, at the moment the bill is not being introduced by the committee itself, and is not expected to be proposed during the hearing.

The committee memo published to frame the hearing outlined the different factors under consideration today: namely, the possible risks posed by stablecoins and the regulatory gaps into which they might fall.

Defining stablecoins

The key question for lawmakers may well boil down to just how they define stablecoins for the purposes of legislation.

In a statement, outgoing Federal Deposit Insurance Corporation Chair Jelena McWilliams said stablecoins could provide faster or more efficient payment tools, but “a key question that the FDIC has been carefully exploring” is whether a stablecoin or its reserves qualify as “deposits” that could be protected by the FDIC.

“These are critical questions with major ramifications for the evolution of stablecoins,” she said. “My personal view is that, generally, bank-issued stablecoins closely resemble digital representations of deposits. I urge the FDIC to build off the work we have done and provide clarity to the public as soon as practicable, which could include promulgating amendments to the deposit insurance rules.”

In McWilliams’ view, a “one-size-fits-all approach” will not work.

The FDIC, Office of the Comptroller of the Currency and Federal Reserve even mentioned stablecoins in its joint statement announcing its crypto policy goals for this year.

America COMPETES

The America COMPETES Act passed out of the House of Representatives with a handful of crypto-related provisions. The big one, which stirred backlash from the crypto industry, could have granted the U.S. Treasury secretary the ability to block crypto transactions to foreign exchanges or persons. The secretary already has this authority, but it’s subject to a 120-day public comment and rulemaking period, giving the public a chance to push back against these restrictions on a case by case basis. This provision was amended by its author, Rep. Jim Himes (D-Conn.) prior to its passage.

The current language still specifies digital assets, but does not remove public notice period or rulemaking requirements, according to Jerry Brito, executive director at Coin Center. In other words, the Treasury secretary would still have to justify blocking any transactions rather than just having the ability to arbitrarily do so.

Another provision targets China’s digital currency plans directly, requiring the secretaries of Treasury and State to publish a report on the dollar’s role as the world reserve currency, analyzing China’s work in becoming “the world’s leading financial center” and the impact if the yuan were to replace the dollar as a global reserve currency.

The provision mentions China’s forthcoming digital yuan and research into a central bank digital currency more broadly several times as a possible risk factor.

Separately, the bill will also direct the Treasury secretary to write and publish a report analyzing cross-border payment systems, including “benefits and concerns” with the existing system. More intriguingly, the report will look at digital currencies and their possible impact.

“The report shall … review and analyze ways in which the Cross Border Interbank Payment Systems (CIPS), cryptocurrencies and foreign central bank digital currencies could erode this system,” the bill said.

Also of interest: A provision directing the National Institute for Science and Technology to research best practices and standards for digital identity management. The director of NIST is further ordered to create a technical roadmap to ultimately enable “the voluntary use and adoption of modern digital identity solutions.”

Next stop: The U.S. Senate.

Tax refunds

Last week, we saw a number of media outlets report the Internal Revenue Service is shifting its guidance on staked crypto assets. Right now these assets are taxed as income when received and potentially face a capital gains tax when they’re transacted away. A couple staking on Tezos sued the IRS last year to recoup their income taxes on claims that they shouldn’t be taxed until they dispose of the asset.

A judge ordered the parties to try and resolve the case outside of court. In December, the IRS offered a refund as part of an apparent settlement. The plaintiffs refused the refund in hopes of securing court precedent.

Several news outlets reported the refund itself as a shift in policy. I’m told that while this is a positive sign for stakers more generally, people should not be reading too much into this move yet because of the specific circumstances here. In other words – it’s cheaper to settle than to continue to litigate.

A spokesperson declined to comment when reached last week.

To be clear, the IRS could still issue guidance in line with the perceived policy shift. It just seems that at this point any assumption that it will seems premature.

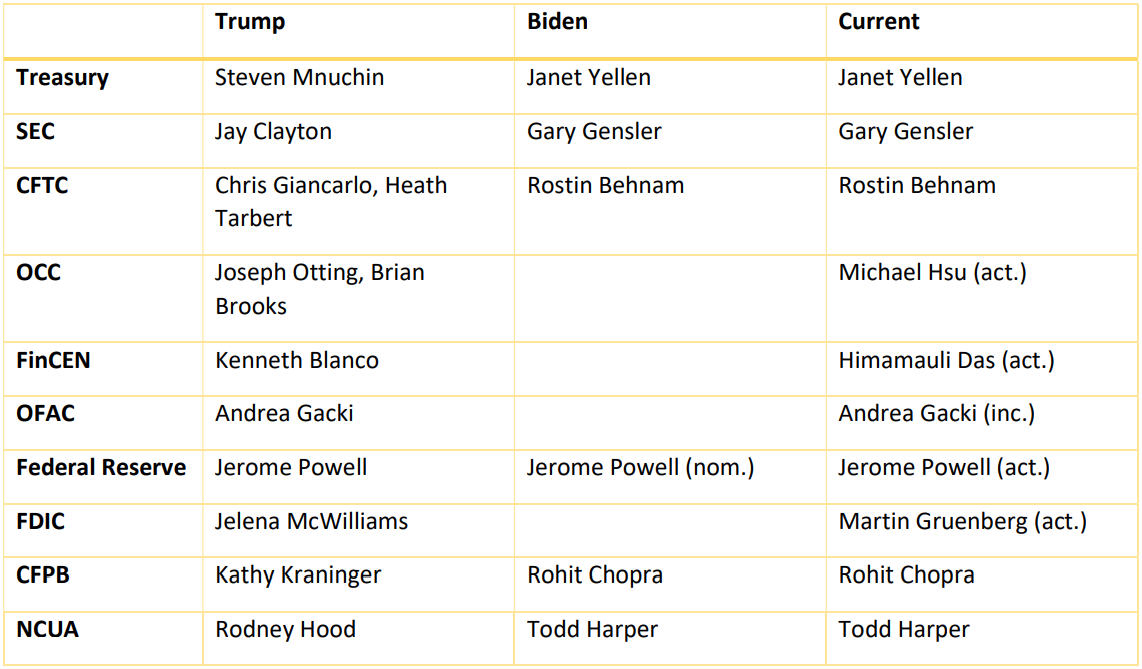

Biden’s rule

Changing of the guard

Key: (nom.) = nominee, (rum.) = rumored, (act.) = acting, (inc.) = incumbent (no replacement anticipated)

Fun fact: Fed Reserve Chair Jerome Powell’s first term expired, but he hasn’t yet been confirmed to his second term. As a result, he’s now Chair Pro Tempore, essentially acting chair until the Senate decides to vote on his renomination heading up the U.S. central bank.

We also now have an acting FDIC chair, after former Chair Jelena McWilliams stepped down on Friday. New Acting Chair Martin Gruenberg (naturally) mentioned that crypto “could pose significant safety and soundness and financial system risks” in his introductory statement.

Elsewhere:

- Of Course It’s OK to Out the BAYC Founders: I think this is a solid take by my colleague Will Gottsegen on this weekend’s Bored Ape Yacht Club news. In brief: Buzzfeed News reporter Katie Notopoulos identified the pseudonymous founders behind Yuga Labs, the business entity that launched the BAYC NFTs. Will argues that Yuga is just like any other massive firm (it might have a $5 billion valuation) and so identifying its founders is fair play. Plus, all it took was a search of publicly available Delaware corporate records.

- Tesla Records $101M Impairment Loss on Bitcoin Holdings for 2021: FASB accounting standards strike again. Tesla recorded a fairly massive loss because the value of the bitcoin it hasn’t sold dropped in value after the electric automaker put the digital asset on its balance sheet. Tesla has not yet sold the bitcoin. Should the value of the bitcoin rise, Tesla cannot report the unrealized gain. I wrote about this like a year ago and whaddya know.

Outside CoinDesk:

- (The Verge) “It’s pronounced ‘neft,’” says The Verge’s Corin Faife.

- (The New York Times) The Times took a look at the U.S.’ sanctions regime and how it might be used to cut Russia off from the global financial system should it invade Ukraine. It starts with the Society for Worldwide Interbank Financial Telecommunications – aka Swift – the infrastructure underpinning global financial firms.

- (The New York Times) The IRS will stop using a facial recognition platform to ID taxpayers, the Times reports. Last week, Business Insider reported the IRS was working with ID.me, a startup that would have had users upload photo IDs, selfies and Social Security numbers to identify themselves. It would then “infer citizenship.” This naturally worried people concerned with what ID.me would do with that information. At the moment, it looks like this partnership is off. Sen. Ron Wyden (D-Ore.), who championed changing the infrastructure bill’s crypto provision last year, called today’s news “big.”

- (ProFootballTalk) This doesn’t have anything to do with crypto, and it’s like the most minor of NFL scandals from last week, but as a long-time fan of the New England Patriots I want to just take a moment to say VINDICATION!! Deflategate was a sham and turns out the NFL knew it. I just hope the league has a harder time covering up its apparent lack of coaching diversity or the Washington Commanders’ alleged egregious harassment of its employees.

If you’ve got thoughts or questions on what I should discuss next week or any other feedback you’d like to share, feel free to email me at [email protected] or find me on Twitter @nikhileshde.

You can also join the group conversation on Telegram.

See ya’ll next week!

DISCLOSURE

Please note that our privacy policy, terms of use, cookies, and do not sell my personal information has been updated.

The leader in news and information on cryptocurrency, digital assets and the future of money, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups. As part of their compensation, certain CoinDesk employees, including editorial employees, may receive exposure to DCG equity in the form of stock appreciation rights, which vest over a multi-year period. CoinDesk journalists are not allowed to purchase stock outright in DCG.

Nikhilesh De is CoinDesk's managing editor for global policy and regulation. He owns marginal amounts of bitcoin and ether.

Nikhilesh De is CoinDesk's managing editor for global policy and regulation. He owns marginal amounts of bitcoin and ether.

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/PK332AQM2RFU3FSZGUBM56SZUI.jpg)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/NCC42C4A2VEGVHTXRSWLCA5EIU.jpg)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/KVE34ILYZVCXDAYYL34VUOBX7U.jpeg)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/4LA4HCFBXBANHBLNPLOES3NZ2I.jpg)